Complete Guide to Building an Overseas Loan System / Thailand Loan System / Small Amount Predatory Loan Source Code (2025 Actual Test)

Complete Guide to Building an Overseas Loan System / Thailand Loan System / Small Amount Predatory Loan Source Code (2025 Actual Test)

To be honest, I once received a project to build an “overseas loan system” where the client requested a small amount predatory loan system for the Southeast Asian market. Honestly, when I first heard this requirement, I was a bit confused, because such systems operate in a gray area of the law, and one misstep could get you into trouble. However, the project fee was quite generous, so I decided to give it a try.

After some research, I discovered that this type of system is essentially a complete loan business process management system, including core modules such as customer management, loan applications, approval workflows, and repayment tracking. However, in some specific markets (such as Thailand, Indonesia, Vietnam), due to relatively lenient regulation, such systems have certain room for survival.

Today, I’ll share the complete process of building this system and my experience of navigating pitfalls, for friends who need it as a reference.

1. System Functionality Overview

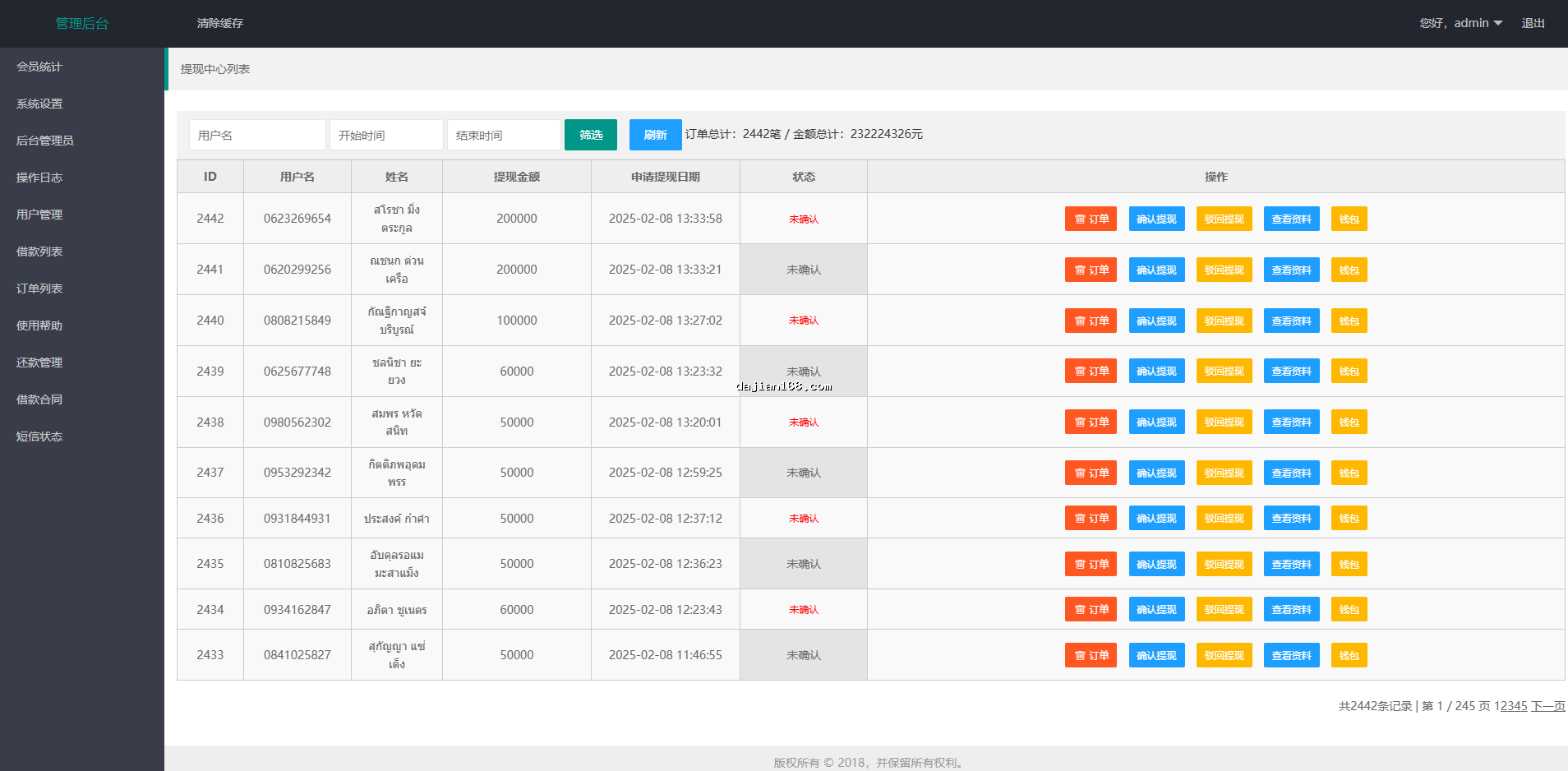

This overseas loan system mainly includes the following core functional modules:

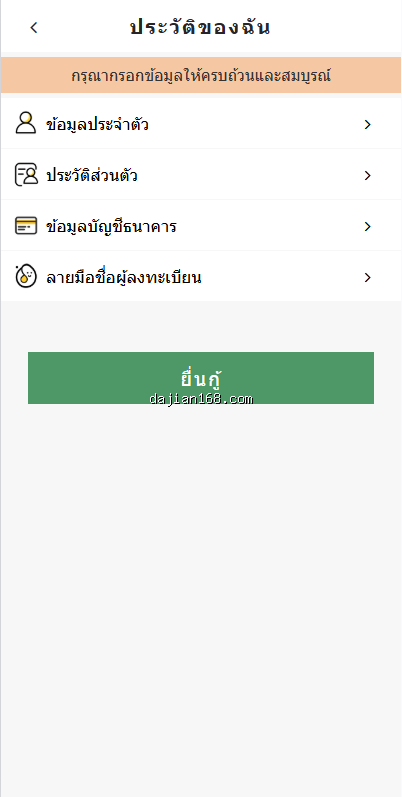

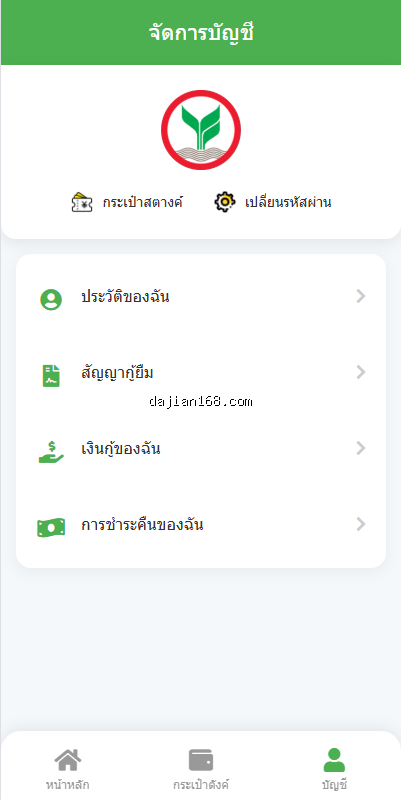

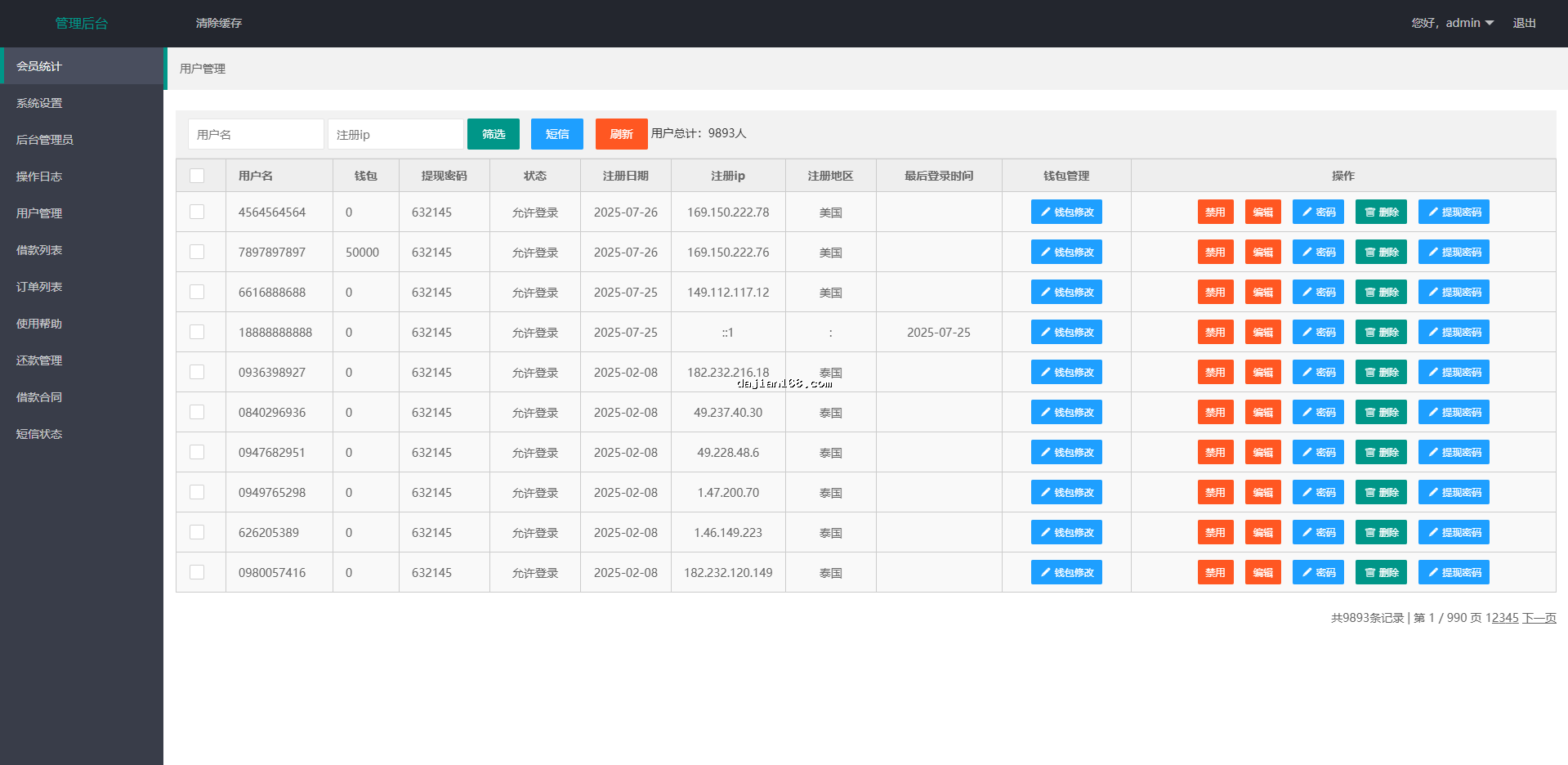

1.1 Customer Management Module

- Customer Information Entry: phone number, ID card, contacts, occupation info, etc.

- Customer Blacklist: automatically identifies high-risk customers

- Customer Segmentation: auto-segments based on credit scores

- Customer Profiling: multi-dimensional data statistical analysis

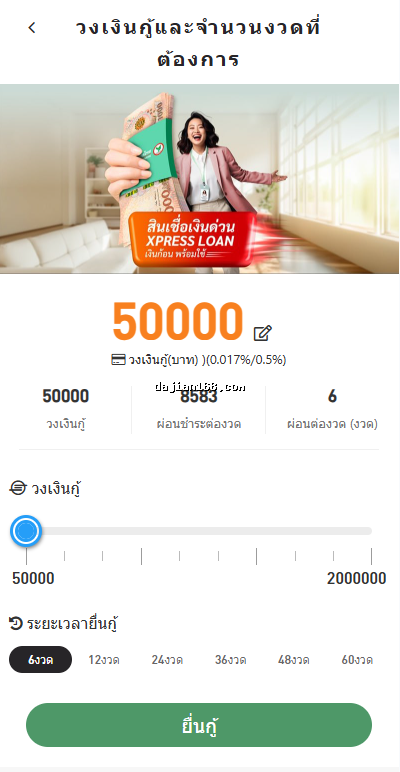

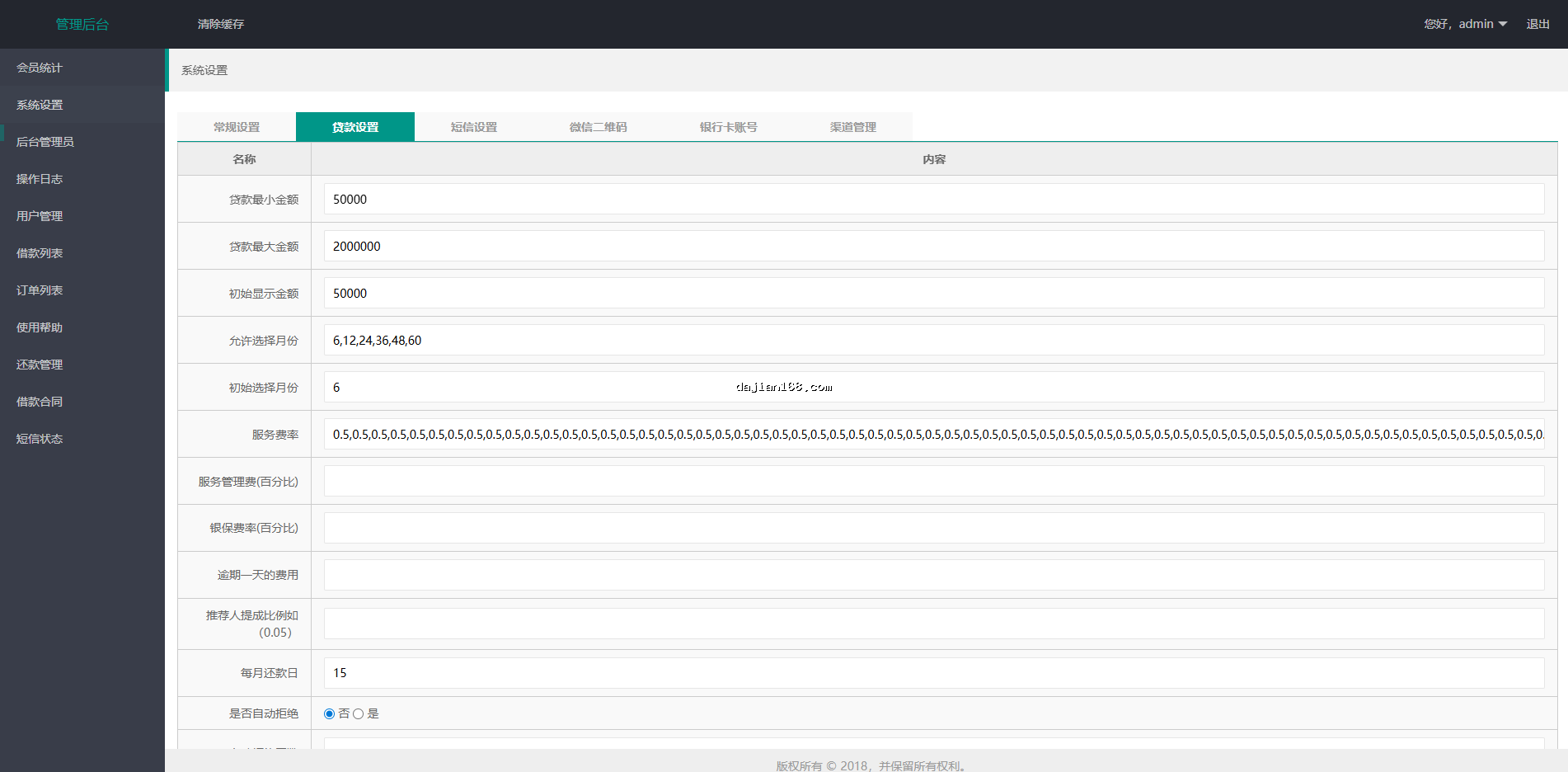

1.2 Loan Application & Approval

- Online Application: supports multi-terminal APP/H5 applications

- Credit Limit Assessment: auto-assesses limits based on customer qualifications

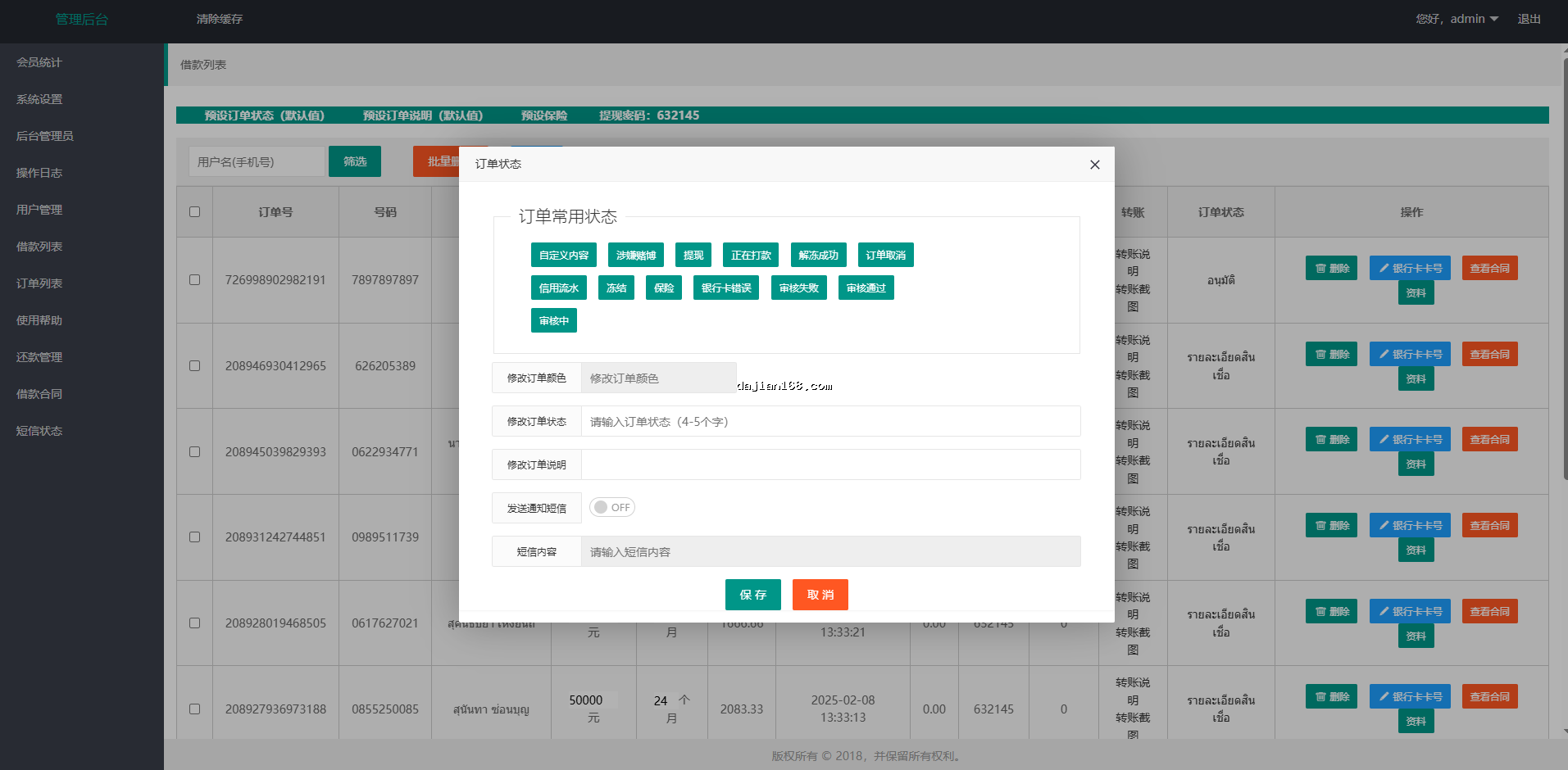

- Risk Control Review: multi-level approval process

- Contract Generation: auto-generates electronic contracts

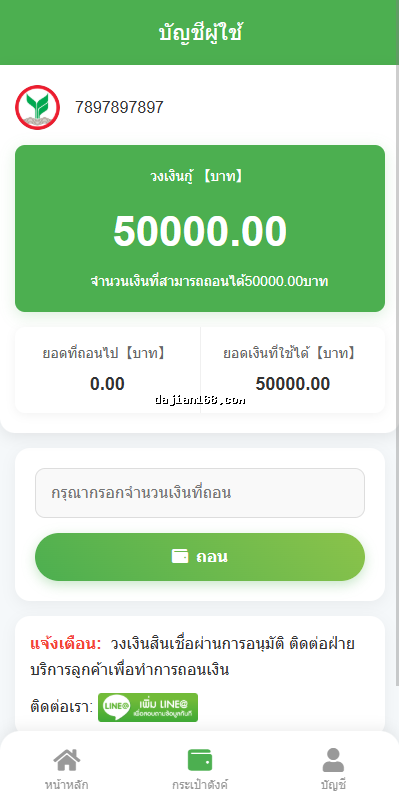

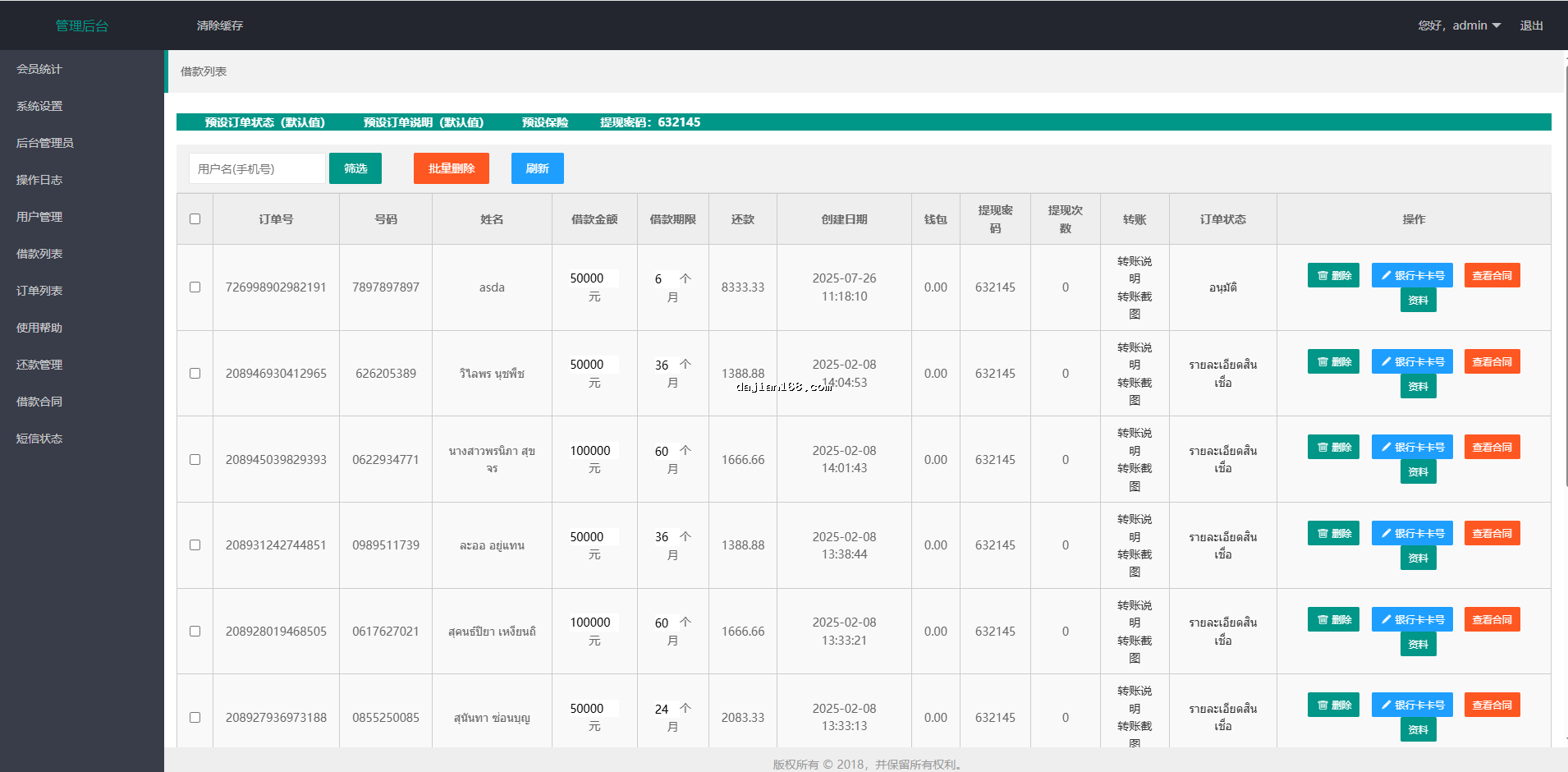

1.3 Repayment Management

- Repayment Schedule: auto-generates repayment calendar

- Auto Debit: integrates with third-party payment systems

- Overdue Reminders: multi-channel smart reminders

- Penalty Calculation: auto-accumulates overdue fees

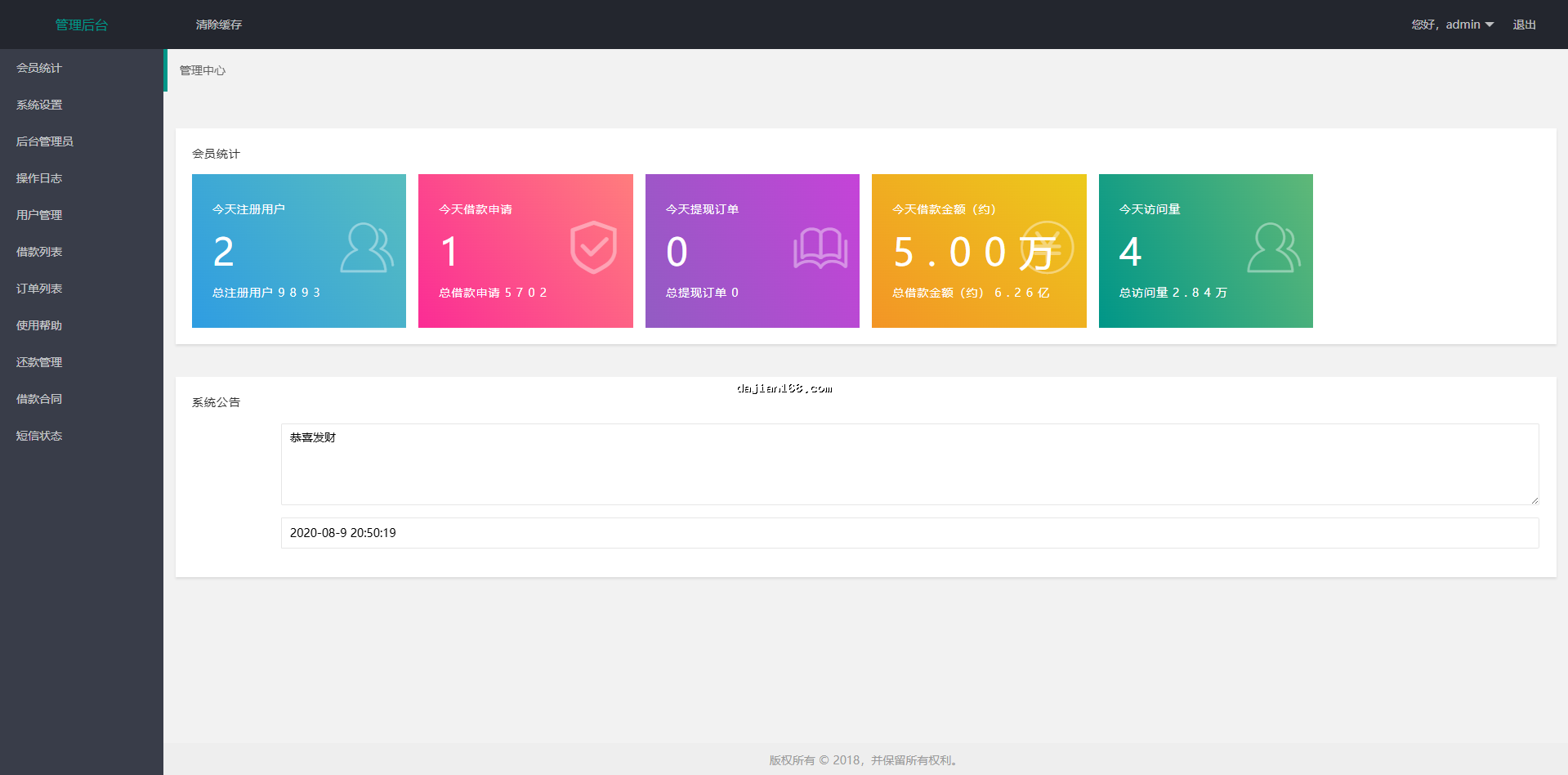

1.4 Statistical Reports

- Lending Statistics: daily, weekly, monthly reports

- Overdue Analysis: multi-dimensional analysis of overdue causes

- Profit Analysis: interest, penalties, operational costs

- Channel Analysis: conversion rates across various channels

⚠️ Important Notice: Before building such a system, please confirm the laws and regulations of your target market. Different countries and regions have vastly different regulatory policies on lending business. It is recommended to consult a professional legal advisor before starting the project.

2. Setup Preparation & Notes

2.1 Environment Setup

- Server: It is recommended to use overseas servers (such as AWS Singapore, Japan nodes) for lower latency and more stable access

- Domain: It is recommended to use .com or .net international domains, avoid using domestic registrars

- SSL Certificate: HTTPS certificate must be installed, some app stores require mandatory HTTPS

- Database: MySQL 8.0+ recommended, be sure to do master-slave backup

- Redis: Used for cache and Session sharing to improve system response speed

2.2 Technology Stack

- Backend: Laravel / Spring Boot / Django are all suitable

- Frontend: uni-app (supports iOS/Android/H5 multi-terminal)

- Database: MySQL + Redis

- Message Queue: RabbitMQ (for processing async tasks)

- File Storage: Alibaba Cloud OSS / AWS S3

2.3 Important Notes

- Payment Interface: It is recommended to use local third-party payments (such as Thailand’s PromptPay, Indonesia’s OVO, etc.)

- SMS Channel: Requires local operator support, it is recommended to find a local service provider

- Data Backup: Full backup at least once a day, off-site backup recommended

- Logging: All sensitive operations must be logged for traceability

3. Common Issues & Pitfalls

Q1: What if overseas server access is slow?

A: This is a very common issue. It is recommended to use CDN acceleration, choose CloudFlare or Alibaba Cloud international CDN, which can effectively improve access speed. Also, choosing a physically closer data center is important—for Southeast Asian markets, Singapore nodes are recommended.

Q2: Payment interface application is difficult, how to solve?

A: Overseas payment interfaces have strict review processes. It is recommended to cooperate with aggregate payment platforms in the early stage, such as Payssion, Paysera, etc., which integrate multiple local payment channels, saving you the trouble of integrating yourself.

Q3: How to handle data compliance issues?

A: Different countries have different requirements for data privacy. Southeast Asian markets should comply with PDPA (Personal Data Protection Act) requirements, while EU markets require GDPR compliance. Technically, you need to implement data encryption, access control, audit logs, and other measures.

Q4: How to handle high concurrency?

A: It is recommended to adopt a microservices architecture, splitting core business into independent services. Use Redis for the caching layer, RabbitMQ for message queues, and database read-write separation. You should also implement interface rate limiting and circuit breaker mechanisms.

4. Custom Solutions

Based on different business scales, I’ve summarized the following custom solutions:

Solution 1: Startup Version (for individuals or small teams)

- Features: Basic loan process + simple risk control

- Concurrency: Supports 500-1000 concurrent users

- Budget: Server + Domain + Payment Interface ≈ 5000-8000 CNY/month

Solution 2: Growth Version (for medium-sized teams)

- Features: Complete business modules + data analysis + multi-channel integration

- Concurrency: Supports 5000-10000 concurrent users

- Budget: Infrastructure + Development ≈ 15000-30000 CNY/month

Solution 3: Enterprise Version (for large organizations)

- Features: All modules + AI risk control + customized requirements

- Concurrency: Supports 10000+ concurrent users

- Budget: Custom development, priced separately

Personal suggestion: If you’re doing this kind of project for the first time, you can start with the Startup Version. Once the business is running smoothly, you can gradually upgrade. After all, the core logic of this system is the same—it’s most important to get the minimum viable product running first.

5. FAQ

Q: How much does this system source code cost?

A: The price of source code on the market varies greatly, ranging from a few thousand to several hundred thousand. It mainly depends on feature completeness and after-sales support. It is recommended to try the demo version first and experience it yourself before deciding.

Q: What qualifications do I need?

A: This is a very critical question. Conducting lending business in most countries requires corresponding financial licenses or filings. It is recommended to first understand the specific requirements of your target market and not to launch blindly.

Q: How to ensure system security?

A: Key points: 1) All data transmission encrypted (TLS); 2) Database encrypted storage; 3) Interface authentication; 4) Regular security audits; 5) Good log tracking.

Q: Is maintenance complicated?

A: It is recommended to choose source code with continuous update support, which will include security patches and feature upgrades in the future. If you maintain it yourself, you need to have a certain technical team.

Q: Can you make Simplified/Traditional Chinese switching?

A: Absolutely possible, it is recommended to use an internationalization framework (i18n) to achieve multi-language support.

Conclusion

To be honest, doing this system really taught me a lot. It not only tests technical ability but also tests your understanding of business processes and risk control. I hope my sharing can help friends who need it.

If you have better experiences or pitfalls you’ve encountered, feel free to exchange in the comments section!

#OverseasLoanSystem #ThailandLoan #SmallAmountLoanSourceCode #FinancialSystemDevelopment #LoanSystemSetup

-

Alipay QR Code Scan

Alipay QR Code Scan

-

WeChat Scan Pay

WeChat Scan Pay