New UI Product Investment Crowdfunding Rebate System Setup Guide: FastAdmin Backend + UniApp Frontend + Three-Level Distribution Full Open Source Deployment

New UI Product Investment Crowdfunding Rebate System Setup Guide: FastAdmin Backend + UniApp Frontend + Three-Level Distribution Full Open Source Deployment

Last month, I built this system for a client doing an overseas wealth management project. It took five or six days of debugging back and forth. To be honest, using the FastAdmin framework for the backend really saved a lot of effort, but there were still a few pitfalls in the interface docking between the uniapp frontend and the backend. This article completely records the setup process and precautions of this Investment Crowdfunding Rebate System for friends who are preparing to start.

One, Detailed System Function Description

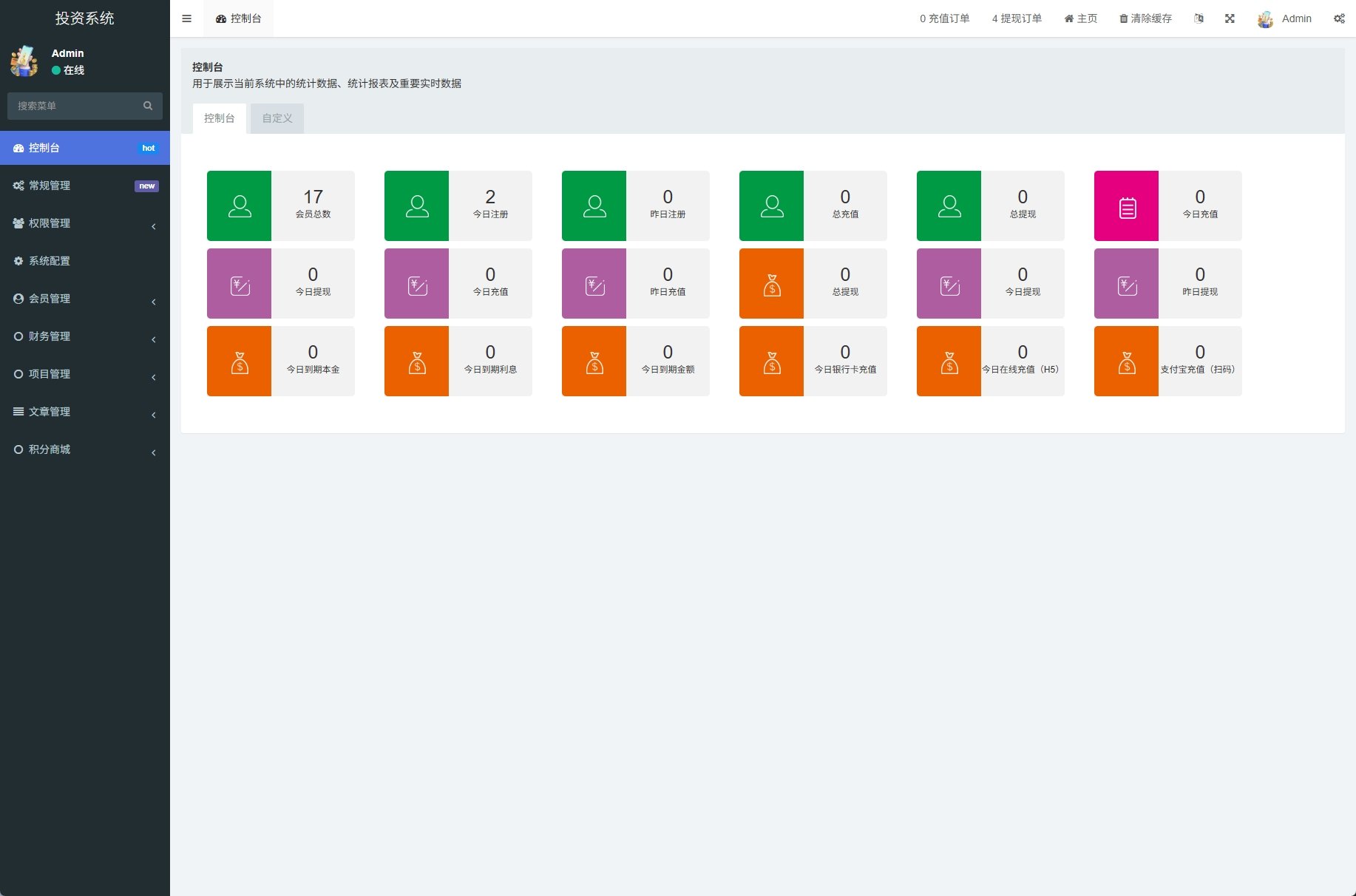

This system is much more complete in functionality than previous versions we have done. Specific modules include:

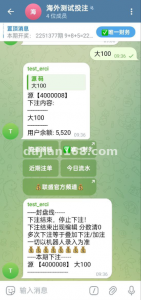

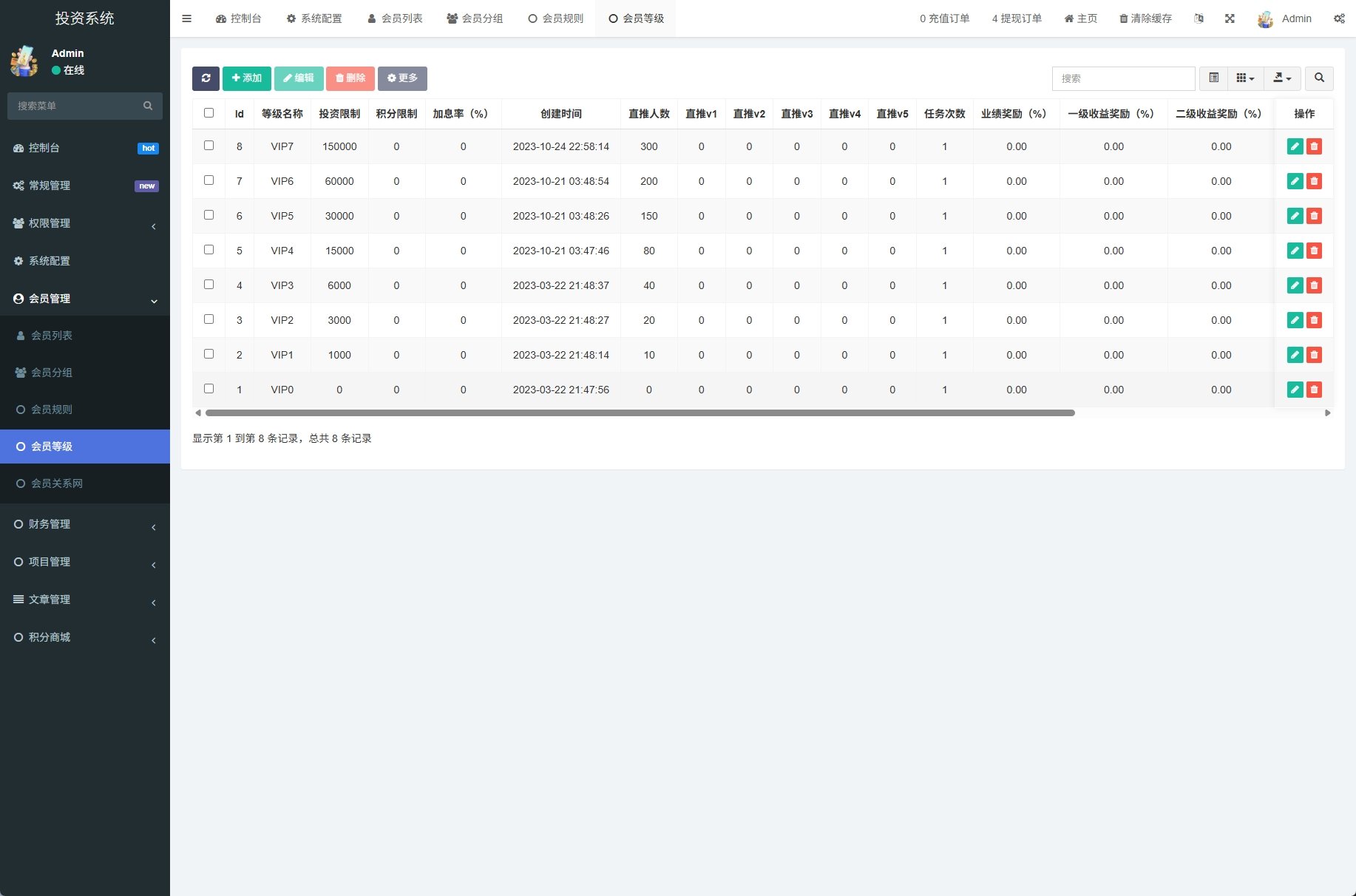

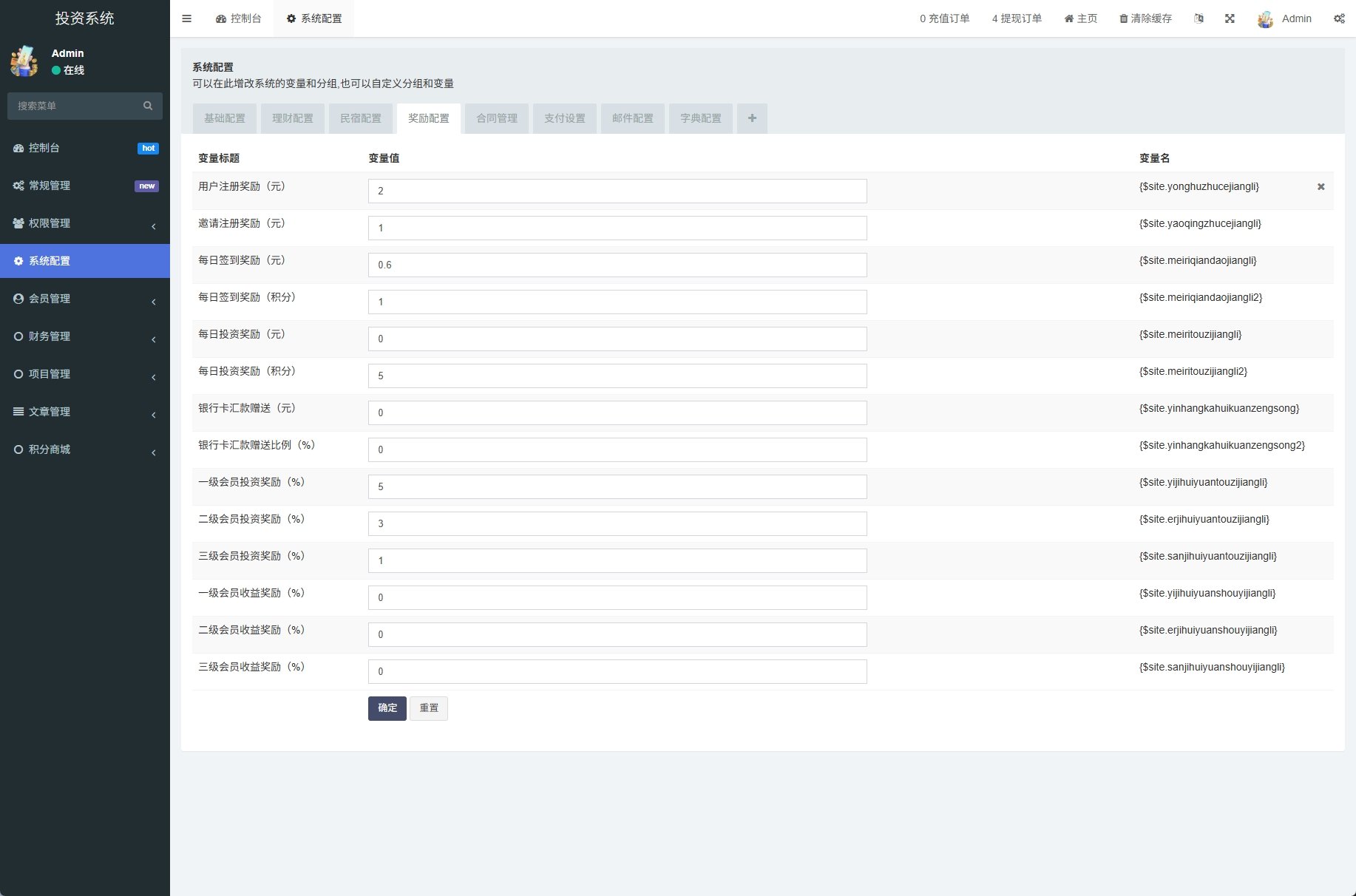

- Flexible Product Configuration: The backend can add, modify, or remove wealth management products at will. Each product has independent settings for investment cycle, daily yield rate, minimum investment amount, and purchase limit. I configured 8 products for the client, with cycles ranging from 7 days to 90 days, and yield rates controlled between 1.5%-3.5%.

- Three-Level Distribution System: After users invite downlines, they can receive first-level, second-level, and third-level commission sharing. The ratio is adjustable in the backend, with a default of 15%-8%-5%. In actual operation, it is recommended not to set the first-level ratio too high, otherwise the platform’s payback period will be too long.

- Daily Sign-In Rewards: Continuous sign-in has tiered rewards, and after breaking the streak, it recalculates. This design is very helpful for retention; after the client went live, daily active users increased by nearly 30%.

- Internal Transfer Function: Users can directly transfer funds between each other without going through payment channels. The handling fee can be set in the backend; it is recommended to set it between 0.5%-1%, which can cover costs without making users反感.

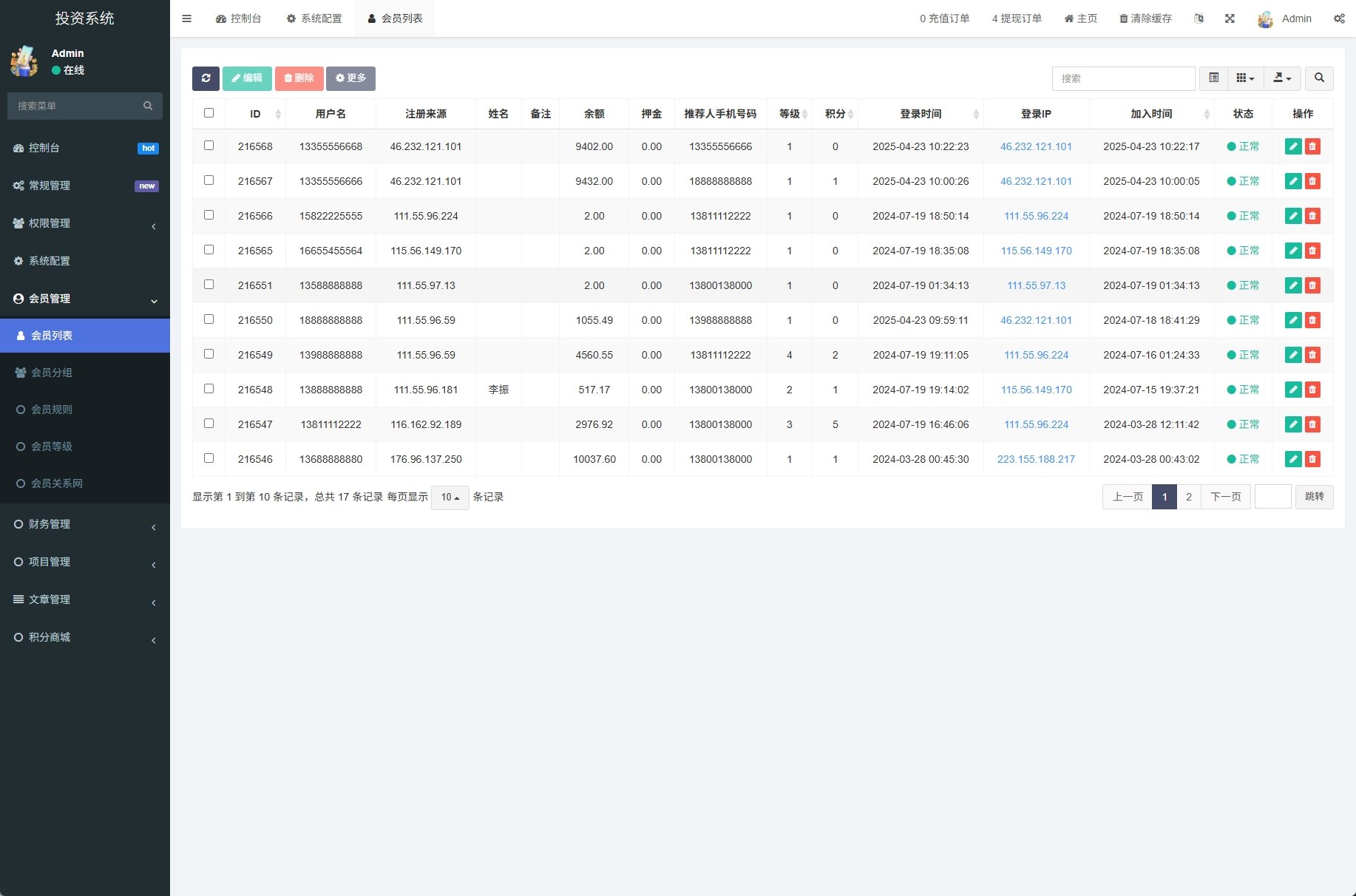

- Recharge and Withdrawal Management: Supports USDT, PayPal, bank cards, and other channels. Each withdrawal requires backend review, and an automatic review threshold can be set (e.g., automatically pass for single transactions below 500 USDT).

- Multi-language Support: The frontend uniapp source code has complete internationalization, supporting not only Chinese and English but also Vietnamese, Thai, and other small languages. Data is not lost when switching languages, and the experience is relatively smooth.

Two, Preparation Checklist Before Setup

Before starting deployment, confirm whether the following environments are in place:

- Server Configuration: It is recommended to start with 4 cores and 8G, with overseas nodes prioritized. If the expected user volume is over 10,000, it is recommended to upgrade to 8 cores and 16G.

- PHP Environment: Must be 7.4+, with GD library, mbstring, openssl, and redis extensions all indispensable. FastAdmin has a dependency on PDO_MYSQL, so don’t forget to install it.

- MySQL 5.7+: When creating the database, choose utf8mb4_general_ci for the character set to avoid garbled text caused by emoji or special characters.

- Composer: FastAdmin relies on third-party packages, so Composer installation is needed.

- Node.js + npm: The uniapp frontend compilation requires it; it is recommended to use Node 16+ version.

- Domain + SSL: Certificates use Certbot for automatic renewal; don’t waste money buying paid certificates.

- Payment Interface: Prepare at least a USDT-TRC20 main channel + a backup channel (e.g., PayPal or Stripe).

There is a detail that is easily overlooked: the FastAdmin installation wizard will create an admin account by default. The password must be changed to a high-strength combination, and the install directory must be deleted immediately after installation is complete. I have seen someone who did not delete the install directory for a week after going live, and as a result, someone directly reset the administrator password.

Three, Common Problems and Pitfall Records

3.1 Excessive Yield Rate Setting Leading to Capital Chain Breakage

The client initially wanted to set a blockbuster product with a 7-day cycle and a 5% daily yield. I persuaded him not to. After calculating: the annualized rate would be 1300%+, and the platform simply couldn’t sustain it. Later, the highest-yield product was controlled to a 90-day cycle with a 120% annualized rate, combined with dynamic allocation of the capital pool, and the cash flow stabilized.

3.2 Three-Level Distribution Mistaken for Pyramid Scheme

Three-level distribution itself is not illegal, but exceeding three levels or setting an entry fee is dangerous. Under legal advice, we adjusted the model to: users register for free, automatically obtain promotion qualifications after investing in any product, and commissions are calculated only based on actual investment amounts, without setting a head fee.

3.3 Sign-In Data Table Expansion Slowing Down Queries

Two months after going live, it was found that the sign-in table had hundreds of thousands of records, and queries were getting slower and slower. Later, a monthly table partitioning mechanism was added, and a joint index was added to user_id and sign_date, and the query speed returned to millisecond level.

3.4 USDT Arrival Callback Delay

The TRON network occasionally gets congested, and USDT arrival time changes from a few seconds to a few minutes. We added a polling mechanism: the frontend displays a “confirming” status, and the backend checks the number of on-chain confirmations every 10 seconds. After reaching 6 confirmations, it automatically releases funds, greatly improving the user experience.

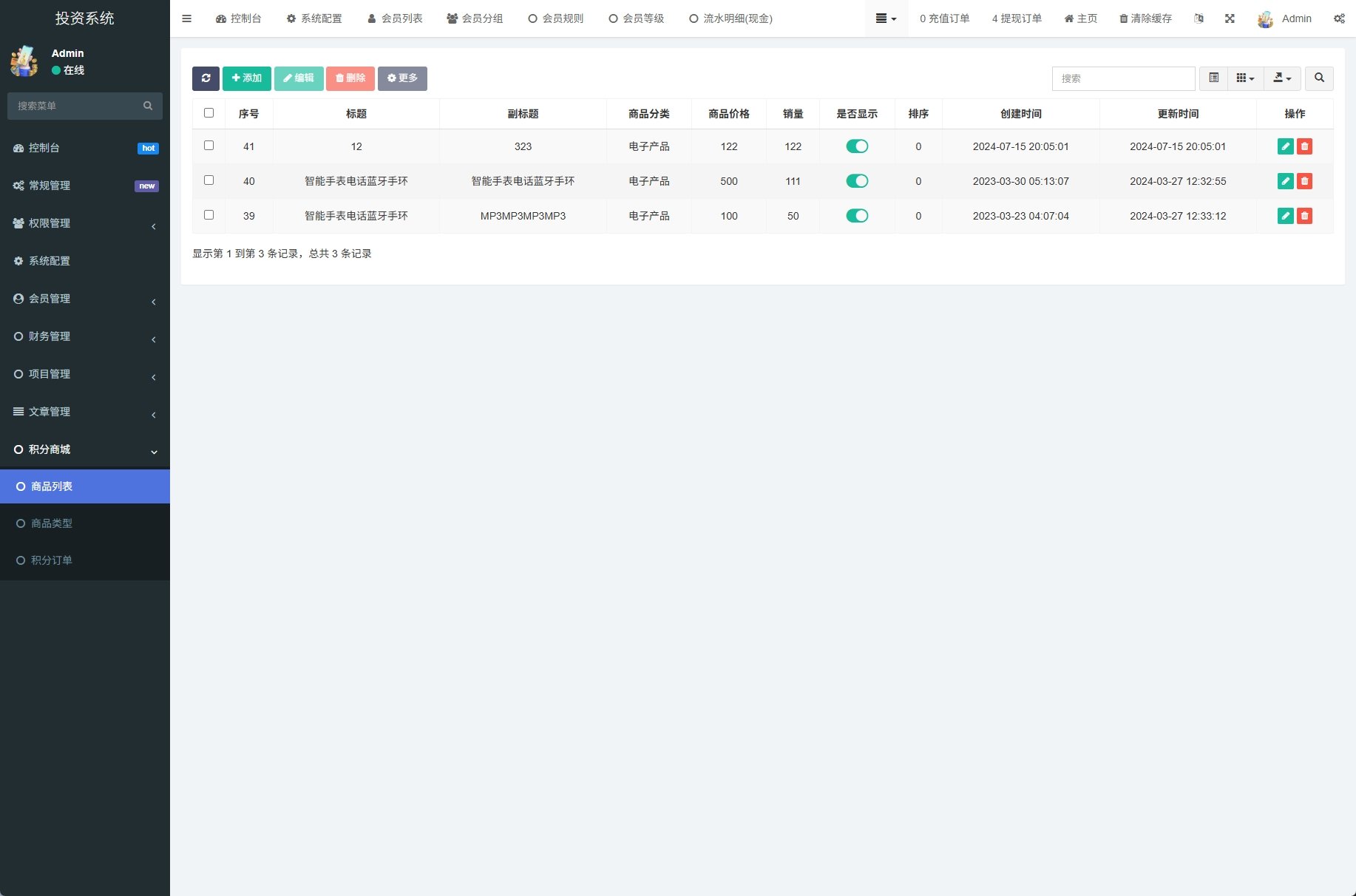

Four, Custom Development Solutions

We have done several secondary developments on this source code. Common requirement directions include:

- Leaderboard Function: Display收益榜, invitation榜, and team榜 to increase user competitive psychology and sense of participation. When doing this, pay attention to data desensitization; don’t expose all real amounts.

- Lock-Up Release Mechanism: After users invest, the principal is released in stages. For example, 30% is released immediately, 40% is released after 30 days, and 30% is released after 60 days. This is used to control the platform’s risk exposure.

- Independent Agent Backend Version: Open a separate backend for big agents, where they can only see their own team’s performance and commissions, and cannot touch the platform’s global data. FastAdmin’s permission module can implement this requirement very well.

- APP Packaging and Listing: The uniapp source code can be directly packaged into APK and IPA, and listed on Google Play or third-party markets. Pay attention to the review rules of different markets; some markets prohibit pure wealth management APPs.

Operational Advice: The essence of an investment rebate platform is capital pool management. If the platform’s real profit sources (such as foreign exchange trading, quantitative arbitrage, advertising placement, etc.) cannot cover user rebate expenditures, then it is a Ponzi scheme. Technology is just a tool for building the platform; whether it can operate long-term depends on whether the business model is viable. Don’t believe in the fantasy that “once the system is stable, you can earn money lying down.”

Five, FAQ Common Questions

Q1: What types of platforms is this system suitable for?

A: The basic architecture is suitable for product crowdfunding, rebate investment, wealth management subscription, pension dividend, and other models. But the specific business type needs to be determined based on your own resources; you cannot copy other people’s play methods directly.

Q2: What are the advantages of using the FastAdmin framework for the backend?

A: FastAdmin is an enhanced version of ThinkPHP, with built-in CRUD generation, permission management, form validation, and other modules. When building this system, 80% of the backend management pages were automatically generated, and only the remaining 20% of business logic needed to be written, resulting in very high development efficiency.

Q3: Is the commission calculation for three-level distribution real-time or periodic settlement?

A: The default is real-time writing to the commission account, but withdrawal requires application review. It can also be changed to a T+1 settlement model, depending on the platform’s cash flow situation. Real-time arrival offers a good user experience, but requires high platform capital reserves.

Q4: How to prevent users from薅签到羊毛?

A: It is recommended to add several restrictions: only one account can be bound to the same device, sign-in requires real-name authentication, continuous sign-in rewards are designed in tiers (small amounts for the first 3 days, big rewards only on the 7th day), and after breaking the streak, it recalculates. This combination can effectively filter out薅羊毛 users.

⚠️ Important Notice: The system setup described in this article is for technical research and study exchange only. Investment rebate and crowdfunding wealth management businesses have different regulatory policies in different countries, and some countries regard them as illegal financial activities. Operators must complete legal compliance review before going live to ensure that the business model complies with local laws and regulations. The technical service provider does not bear any operational risks.

#Investment Crowdfunding Rebate System #FastAdmin Framework #Three-Level Distribution Source Code #UniApp Wealth Management System #Crowdfunding Rebate Platform

-

Alipay QR Code Scan

Alipay QR Code Scan

-

WeChat Scan Pay

WeChat Scan Pay